Optimizing the Advantages of Home Loans: A Step-by-Step Method to Safeguarding Your Perfect Residential Property

Navigating the complicated landscape of home car loans needs a methodical approach to ensure that you protect the home that straightens with your monetary objectives. By starting with a detailed assessment of your economic placement, you can recognize one of the most suitable financing alternatives offered to you. Comprehending the nuances of different lending types and preparing a thorough application can considerably affect your success. The ins and outs don't end there; the closing process demands equal focus to detail. To truly take full advantage of the benefits of home mortgage, one must consider what steps follow this foundational job.

Comprehending Home Lending Basics

Comprehending the principles of home loans is vital for anybody considering acquiring a residential property. A home mortgage, frequently referred to as a mortgage, is a financial item that allows individuals to obtain money to buy property. The borrower agrees to repay the finance over a specified term, usually varying from 15 to 30 years, with passion.

Key parts of home mortgage include the major amount, rate of interest prices, and repayment timetables. The principal is the quantity obtained, while the passion is the cost of borrowing that amount, shared as a portion. Passion rates can be fixed, continuing to be consistent throughout the lending term, or variable, changing based on market problems.

In addition, borrowers need to know different types of home loans, such as traditional fundings, FHA finances, and VA financings, each with unique eligibility criteria and benefits. Recognizing terms such as down payment, loan-to-value proportion, and personal home loan insurance coverage (PMI) is also essential for making educated choices. By realizing these essentials, potential home owners can navigate the intricacies of the home loan market and determine alternatives that align with their financial goals and property desires.

Assessing Your Financial Scenario

Assessing your economic circumstance is a vital step before getting started on the home-buying trip. This assessment involves a comprehensive assessment of your earnings, costs, cost savings, and existing debts. Begin by calculating your total month-to-month income, including incomes, perks, and any additional resources of earnings. Next, listing all monthly costs, making certain to represent dealt with expenses like rent, utilities, and variable costs such as groceries and amusement.

After developing your revenue and expenditures, establish your debt-to-income (DTI) proportion, which is essential for lenders. This proportion is calculated by dividing your total month-to-month financial obligation repayments by your gross month-to-month revenue. A DTI proportion below 36% is normally taken into consideration desirable, indicating that you are not over-leveraged.

In addition, examine your credit history, as it plays a pivotal function in safeguarding positive finance terms. A greater credit history can bring about reduced rates of interest, ultimately conserving you cash over the life of the finance.

Checking Out Loan Options

With a clear image of your economic situation established, the next action includes checking out the numerous financing alternatives available to news prospective homeowners. Recognizing the various kinds of home mortgage is critical in choosing the appropriate one for your demands.

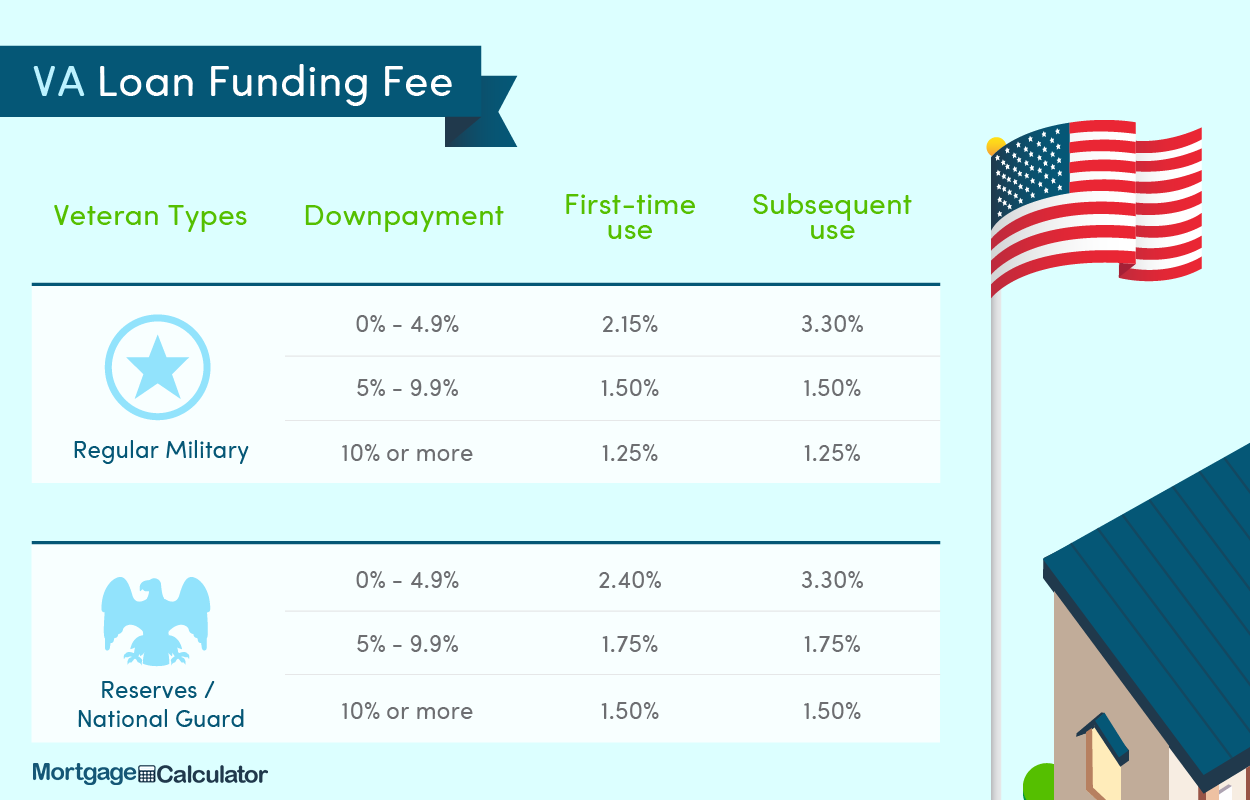

Standard finances are conventional financing techniques that typically need a greater credit rating and down payment yet offer competitive rates of interest. Conversely, government-backed lendings, such as FHA, VA, and USDA finances, deal with specific teams and often call for lower down payments and credit history, making them available for first-time customers or those with minimal funds.

One more option is variable-rate mortgages (ARMs), which feature reduced preliminary rates that adjust after a specific period, possibly bring about considerable financial savings. Fixed-rate home loans, on the other hand, offer stability with a constant interest price throughout the car loan term, protecting you versus market fluctuations.

In addition, consider the funding term, which typically ranges from 15 to three decades. Shorter terms may have greater month-to-month payments yet can save you rate of interest over time. By very carefully reviewing these alternatives, you can make an informed decision that lines up with your financial objectives and homeownership ambitions.

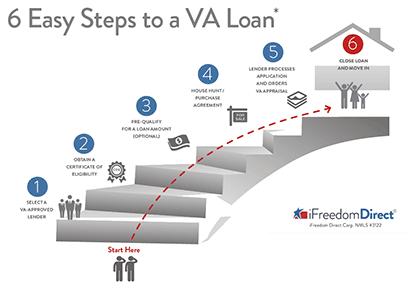

Planning For the Application

Efficiently preparing for the application procedure is necessary for safeguarding a home financing. A strong debt score is essential, as it affects the lending amount and passion prices look at here available to you.

Organizing these papers in breakthrough can significantly quicken the application procedure. This not only gives a clear understanding of your loaning ability but additionally reinforces your placement when making a deal on a residential or commercial property.

Moreover, establish your budget by factoring in not simply the funding amount but additionally residential property taxes, insurance, and maintenance costs. Acquaint on your own with different loan kinds and their corresponding terms, as this expertise will equip you to make educated choices during the application process. By taking these proactive steps, you will enhance your readiness and boost your possibilities of securing the home mortgage that best fits your requirements.

Closing the Deal

During the closing meeting, you will examine and authorize various records, such as the lending estimate, closing disclosure, and mortgage contract. It is essential to completely recognize these papers, as they detail the lending terms, payment routine, and closing costs. Take the time to ask your loan provider or property representative any type of questions you may need to avoid misconceptions.

When all files are signed and funds are moved, you will get the tricks to your new home. Bear in mind, closing expenses can differ, so be planned for expenses that might include evaluation fees, title insurance policy, and attorney fees - VA Home Loans. By staying organized and educated throughout this procedure, you can ensure a smooth shift right into homeownership, making best use of the advantages this post of your home car loan

Conclusion

In final thought, making the most of the advantages of home finances demands an organized approach, incorporating a thorough assessment of economic circumstances, exploration of varied finance alternatives, and careful preparation for the application process. By adhering to these actions, possible property owners can enhance their opportunities of securing beneficial financing and attaining their property possession objectives. Eventually, careful navigating of the closing process better strengthens a successful transition into homeownership, making sure lasting monetary security and contentment.

Browsing the facility landscape of home car loans calls for a methodical technique to ensure that you secure the residential property that aligns with your economic goals.Understanding the basics of home financings is important for any person taking into consideration buying a building - VA Home Loans. A home financing, typically referred to as a mortgage, is a financial product that permits individuals to borrow cash to acquire genuine estate.In addition, borrowers ought to be aware of various kinds of home loans, such as traditional finances, FHA financings, and VA fundings, each with distinct qualification standards and advantages.In conclusion, taking full advantage of the benefits of home lendings requires a systematic technique, including a thorough evaluation of monetary situations, exploration of diverse financing alternatives, and precise preparation for the application process